Know Before You Close.

Simple Answers To Your Questions About The CFPB.

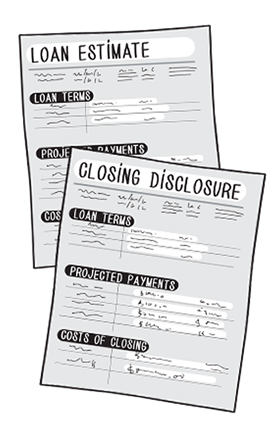

Currently, borrowers receive two separate forms from their lender at the beginning of the transaction: the Good Faith Estimate (GFE), a form required under the Real Estate Settlement Procedures Act (RESPA), and the initial disclosure required under the Truth-in-Lending Act (TILA). For loan applications taken on or after October 3rd, 2015 the creditor will instead use a combined Loan Estimate form intended to replace the two previous forms. The new three-page Loan Estimate form must be provided to borrowers on a timetable similar to the current receipt of the GFE.

The combination of forms continues at the end of the transaction as well, with the HUD-1 Settlement Statement and the final TILA forms now combined into a single Closing Disclosure form. This new five-page form is used not only to disclose many terms and provisions of the loan, but also the financial transaction of the closing of the sale.